Another risk to the US government is a change in the denomination of commodities, such as crude oil. If OPEC decides to adopt, for example, the euro to denominate crude oil, then the eurozone economies would no longer need to hold such large reserves of dollar assets. They would no longer have to worry about exchange rate fluctuations affecting the price of crude oil and no longer need to hedge against this risk. This would result in a significant reduction in the number of buyers of US Treasuries.

In 1998, Saddam Hussein, the former President of Iraq and former head of the oil industry, tried to do just that. He announced that Iraqi oil would be denominated in euros, not dollars. Fortunately for the US, this practice did not extend to other countries and regions outside of Iraq. But to make sure that this practice would never spread in the future, the US government changed the way Iraqi crude oil was denominated back to the US dollar as the denomination currency after it took control of Iraq in 2003. However, the possibility of OPEC or some other large oil producer changing this practice in the future is not ruled out. If anyone makes such a change, you can expect to see a reaction from the market.

To see how the market would react to the threat of falling demand for US Treasuries, you need only look at the reaction of the EUR/USD when the Central Bank of the Russian Federation changed its foreign exchange reserve policy on 19 March 2005. At that time, the Central Bank of the Russian Federation had adjusted its foreign exchange reserve structure from approximately 90% US dollars plus 10% euros to 80% US dollars plus 20% euros. In the weeks that followed, the EUR/USD was seen to “slam on the brakes” after its previous sharp decline and then move sideways as below.

The impact of this Russian move did not last long, however, as investors began to realise that the news was not as significant as it had been at the time. However, it does illustrate how sensitive the foreign exchange market is to such risks. Even though the market will eventually filter this information and decide that it is not significant, it will still give investors pause until they have sorted themselves out before acting again.

Although this policy issued by the Central Bank of the Russian Federation has had only a small impact, such policies announced by other central banks in the future will not be so simple. Such policies are bound to emerge, as many central banks have already issued reports and statements on the subject to test the waters. As globalization continues to turn the world into a more connected web, foreign central banks are bound to diversify their foreign exchange reserves to reduce their dependence on the US government and economy. When that happens, be prepared to reap the rewards of the forex market.

Fundamental analysis tool: International capital flows data

As you can imagine, the US government is very concerned about who is buying US Treasuries and how many US Treasuries are held by each purchaser. In order to fully understand this information, the US Treasury tracks and catalogues this information. Ultimately it is through the International Capital Flows System that the above is done. The international capital flow data tells us how many Treasuries the US government has sold, who has purchased them and how many US Treasuries are held by these purchasers in total.

By observed the trends in international capital flow data, you can expect the US dollar to make changes in the future. The US Treasury usually releases international capital flows data at 9 am Eastern Time on the 11th business day of each month. Remember, you don’t need to worry about whether foreign investors are investing more or less in US Treasuries, it has no impact on your ability to make money in the forex market. All you need to do is watch it fluctuate.

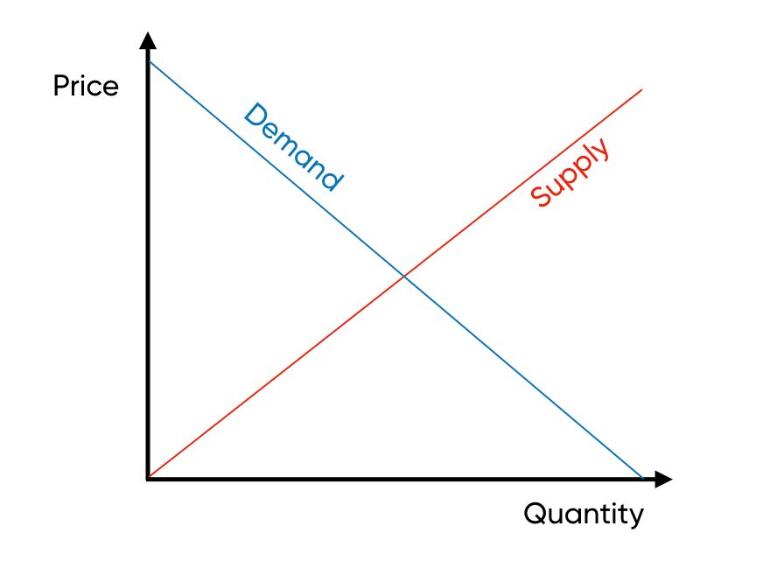

Below are a few graphs that show how changes in international capital flow data would be reflected in changes in the supply and demand graph for the dollar. The first is the basic supply and demand diagram as shown below.

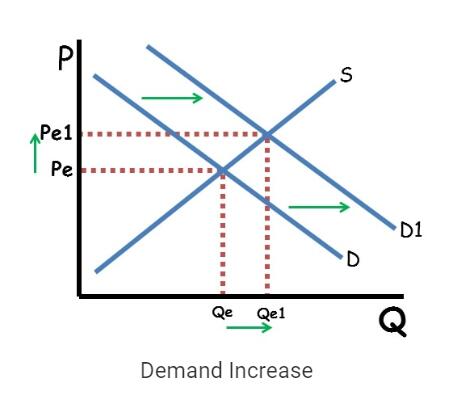

You know the demand for dollars has increased when international capital flow data shows an increase in purchases of US Treasuries by foreign governments and other investors who must use dollars to buy US Treasuries. When the demand for dollars increases, the value of the dollar rises. You can see in the chart below how the price level of the dollar will change when our demand for dollars increases.

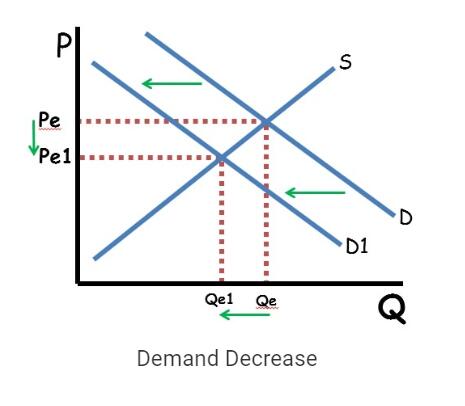

You know there is less demand for the dollar when data on international capital flows show that foreign governments and other investors are buying fewer US Treasuries. When market demand for the dollar decreases, the value of the dollar falls. You can see in the chart below how the price level of the dollar will change when we have less demand for it.

Let’s look at an example of how the foreign exchange market reacts to international capital flow data, as shown in the chart below. Between 2000 and 2001, the US dollar strengthened relative to the Japanese yen. This meant that the Japanese government, one of the largest overseas holders of dollar assets, was less interested in buying US Treasuries when the dollar strengthened. And at this time the Japanese government did not need to do anything to reduce the value of the yen. You can see from the international capital flows data that the rate of Japanese purchases of US Treasuries is actually decreasing, and the total holdings are also decreasing.

In contrast, when the US economy slowed down after 2002, the dollar began to depreciate. This is never good news for an export-oriented country like Japan, as a weaker dollar leaves fewer foreign goods available for US consumers to buy. So in order to keep the yen at an exchange rate level favourable to the Japanese economy, the Japanese government began to increase the amount of US Treasury bonds it purchased. The chart below shows the reaction of the foreign exchange market at that time.

What we are looking for as forex traders are confirmation of the current trend in the dollar from foreign governments. If the US keeps getting stronger and you find that foreign governments, such as Japan, have reduced the proportion of their investments in US dollar assets, you know that these governments believe that the current upward trend in the US dollar will continue. And vice versa. If the dollar keeps weakening and you see foreign governments increasing their investment ratio in dollar assets, you know that these governments believe that the current downward trend in the dollar will continue.